picture alliance / ASSOCIATED PRESS / Markus Schreiber

Tracker

Economic Indicators

China’s economy ends the year on a weak footing

MERICS Economic Indicators Q4/2023

MERICS Q4 analysis: China’s economy ends 2023 weak and facing multiple challenges as it slowly reshapes

Hopes were high that the end of zero-Covid lockdowns in late 2022 would bring China’s economy roaring back to life in 2023 and give the battered world economy a much-needed boost. This optimism had already begun to fade in the first half of the year as economic recovery was hampered by subdued consumption and the real estate sector's drag on growth. Despite the slight uptick in GDP growth in the last quarter of 2023, rising to 5.2 percent, up from 4.9 percent in Q3, the economy is ending the year on a weak footing. In a speech at Davos, Premier Li Qiang told the World Economic Forum that the Chinese economy’s present difficulties felt like “hiking in the Alps”, even though - in his view - it was fundamentally strong.

Annual GDP growth also came in at 5.2 percent, so China achieved its GDP growth target of “around 5 percent”. But base effects from low 2022 growth made the economy appear stronger than it is. Forced withdrawal from the country’s decade long real estate investment addiction is causing financial aftershocks, sending ripple effects throughout the economy. Real estate developers are on the verge of a liquidity crisis, causing stress throughout the financial sector, while shadow bank Zhongzhi Enterprise Group declared insolvency in November and bankruptcy in January.

The People's Bank of China (PBOC) responded by signaling emergency liquidity support for vulnerable smaller banks and urging assistance to highly leveraged local governments. While a full-blown financial crisis is currently unlikely, monetary policy is actively engaged in managing risks. It is no wonder that, in such an environment, household sentiment remains stuck at record lows. Efforts to shore up the mood faltered over the last quarter of 2023. Weak consumption pulled China into deflation in Q4 amid deep-seated insecurity caused by real estate worries and weak employment.

The government continues to roll out new measures to stabilize the economy. Following years of crackdowns and regulations, it is opting for more pro-business policies. The 31-point plan issued in July was complemented by a 25-point plan in November, aiming to reduce bureaucracy, provide tax relief, support new hiring, and facilitate cheaper financing. But the measures do not signal a significant shift in policy priorities. The strategic focus remains on redirecting funds from non-strategic sectors, like real estate, to bolstering manufacturing and technological capabilities. But this also means economic growth is benefiting a narrower portion of society and businesses.

Geopolitical frictions are likely to further impact the direction of China’s economy. Over the final quarter, new policy developments in China and from the United States and European Union presaged further deteriorating trade relations. Fears of Chinese state subsidies and overcapacities impacting the global market are growing in advanced economies, which see their manufacturing industries under threat. The EU's probe into subsidies for Chinese EVs makers and China's retaliation with a probe into European brandy served as an early warning. Efforts to enhance economic security could trigger further tit-for-tat actions on export and investment restrictions, complicating the global economic landscape.

2024 looks sure to be a challenging year for China’s economy. Pressure on the leadership’s economic policies will mount, as public dissatisfaction is only likely to increase unless the situation significantly improves for private households. But in a complicated geopolitical environment a significant change of course seems unlikely.

The MERICS China Confidence Index (MCCI)

The MERICS China Confidence Index measures household and business confidence in future income and revenues. The index is weighted between household and business indicators. It includes the following indicators: stock market turnover, future income confidence, international air travel, new manufacturing orders, new business in the service sector, urban households’ house purchase plans, venture capital investments, private fixed asset investments and disposable income as a share of household consumption. All components have been tested for trends and seasonality.

The MCCI was first developed in Q1 2017.

The MERICS China Confidence Index measures household and business confidence in future income and revenues. The index is weighted between household and business indicators. It includes the following indicators: stock market turnover, future income confidence, international air travel, new manufacturing orders, new business in the service sector, urban households’ house purchase plans, venture capital investments, private fixed asset investments and disposable income as a share of household consumption. All components have been tested for trends and seasonality.

The MCCI was first developed in Q1 2017.

![]() Hover over/tap the charts to see more details.

Hover over/tap the charts to see more details.

Exhibit 1

Macroeconomics: GDP growth is on target but cannot mask underlying weaknesses

Exhibit 2

![]() Hover over/tap the charts to see more details.

Hover over/tap the charts to see more details.

Exhibit 3

- GDP expanded by 5.2 percent in the final quarter of 2023, up from 4.9 percent in Q3. Annual growth was also 5.2 percent (see exhibit 2), meaning China reached its 2023 growth target of “around 5 percent”. However, the improvement in Q4 can be attributed to comparison with weak growth in the last quarter of 2022 when the sudden end of zero-Covid lockdowns produced a wave of infections.

- The recalibration of China’s growth model is progressing as the real estate sector’s weight in the economy is being downsized. The shift towards the “real economy”- manufacturing and innovation – is in full swing. But this also means that economic growth is benefiting a smaller section of society and negatively affecting income distribution.

- The shift can be seen in government tax revenues. Stamp duty revenue from real estate sales further deteriorated over the final quarter of 2023, contracting by 12.2 percent in the months to November (latest available data) compared to the same period of 2022 (see exhibit 3). Consumption and corporate income tax did not fare much better and continued to contract.

- Exports' contribution to GDP is easing after soaring exports gave the economy a much-needed boost over the pandemic. After reaching 19.8 percent of GDP in 2022, a level not seen since 2015, their share of growth fell to 19 percent in 2023. A gradual decline is expected in 2024, so a stronger rebound in domestic consumption will be critical for overall growth.

- Going into 2024, China’s economy is not in crisis, nor is it on a stable footing. Weaker external demand and potential escalating trade frictions as well as looming deflation and risks in the highly leveraged financial system all mean China faces formidable headwinds.

What to watch: The government’s policy direction will become more contested if growth does not stabilize in the first half of 2024.

Business: Manufacturing grew steadily over Q4 but weak new orders hint at trouble

Exhibit 4

![]() Hover over/tap the charts to see more details.

Hover over/tap the charts to see more details.

Exhibit 5

- Value-added production jumped to 6.8 percent in December from 4.5 percent at end of Q3 year on year, though the data benefited from low base levels in late 2022 when Covid-19 swept the country and dampened factory output. But industrial output growth improved steadily over 2023, gradually increasing from a low of 2.4 percent to 4.3 percent in December on a year-to-date basis.

- Stronger manufacturing activity was the most important growth driver. Growth steadily increased during Q4 to 7.1 percent growth in December year on year, the highest level in 2023 (see exhibit 4). Growth rates in key manufacturing sectors were all either higher than, or close to, double digits in December, including automobiles (13 percent), chemicals (9.6 percent), and electrical machinery (12.9 percent).

- Industrial capacity utilization reached its highest level since in two years. The total industrial utilization rate rose by 0.2 points in Q4 on the previous quarter, reaching 75.9 percent. Within manufacturing, automobile (3.7 points) and chemical fiber production (6.5 points) recorded the biggest quarterly jumps, reaching 76.9 and 85.7 respectively in Q4.

- Output of EV’s continued to surge, growing by 43.7 percent in December to make up 37.5 percent of passenger vehicles produced. However, output of construction-related inputs continued to contract, including crude steel (-14.9 percent) and pig iron (-11.8 percent).

- The Purchasing Managers’ Index (PMI) revealed that companies’ business expectations began to soften again during Q4 after previous steady improvements in new orders, including export orders (see exhibit 5). As a result, the order backlog has also dropped to the lowest level in 12 months.

- Companies’ profits improved throughout the year though they continued to fall. Operating profits of companies fell by 4.4 percent in November (latest data available), better than the 9 percent contraction at the end of Q3. Falling factory prices are undermining profitability, putting some companies, especially small and medium sized companies, at risk of running out of liquidity.

What to watch: Companies’ business expectations remain tainted by uncertainty and weaker new orders may point to slower growth ahead.

International trade and investment: China's exports showed signs of a fragile recovery in Q4 at the end of a weak year

Exhibit 6

![]() Hover over/tap the charts to see more details.

Hover over/tap the charts to see more details.

Exhibit 7

- Exports retuned to growth over the final quarter of 2024 after six consecutive months of contraction. They expanded 0.5 percent year on year on a USD basis in November and 2.3 percent in December. The recovery beat market expectations but was largely due to base effects from the sharp drop in exports at the end of 2022 when China has hit by a wave of Covid-19.

- But there are faint signs of improvement as exports to key markets jumped in December. Although lower on a year-on-year basis, China’s exports to the EU and ASEAN measured by USD value significantly improved on a monthly basis, regaining figures last seen earlier in the year. These fragile gains fueled hopes that global demand will pick up further (see exhibit 6).

- Base effects also helped imports return to growth in December, expanding by 0.2 percent. Q4 began with an expansion of 3 percent in October and turned into the year’s strongest quarter for import growth. But sluggish demand meant imports contracted nine times in 2023 and fell by 5.5 percent annually.

- Imports of integrated circuits, critical for China’s massive electronics industry, improved in December, expanding by 5.9 percent year on year. But annually imports were down by 15.4 percent. However, imports of semiconductor equipment doubled year on year in December and remain close to the record levels seen in September as export restrictions loom.

- While annual exports contracted for the first time since 2016, the dip came after strong growth since the pandemic. China’s trade surplus is more than double the 2019 level (see exhibit 7). In 2023, China’s trade balance reached 823.3 billion USD, just below the 2022 record of 837.9 billion USD. Concerns about China’s industrial overcapacities being exported to stimulate growth are rising in other countries.

- Trade frictions escalated in Q4, with an EU probe into Chinese EV subsidies and tighter semiconductor-related restrictions from the United States. China responded with controls on graphite and an investigation into European brandy. In 2024, things may get worse and risk disruptions to trade.

What to watch: Trade figures in March following the Chinese New Year holiday in mid-February will provide an indication of whether the recovery is on a more solid footing.

Financial markets: Monetary policy support ramped up to boost growth

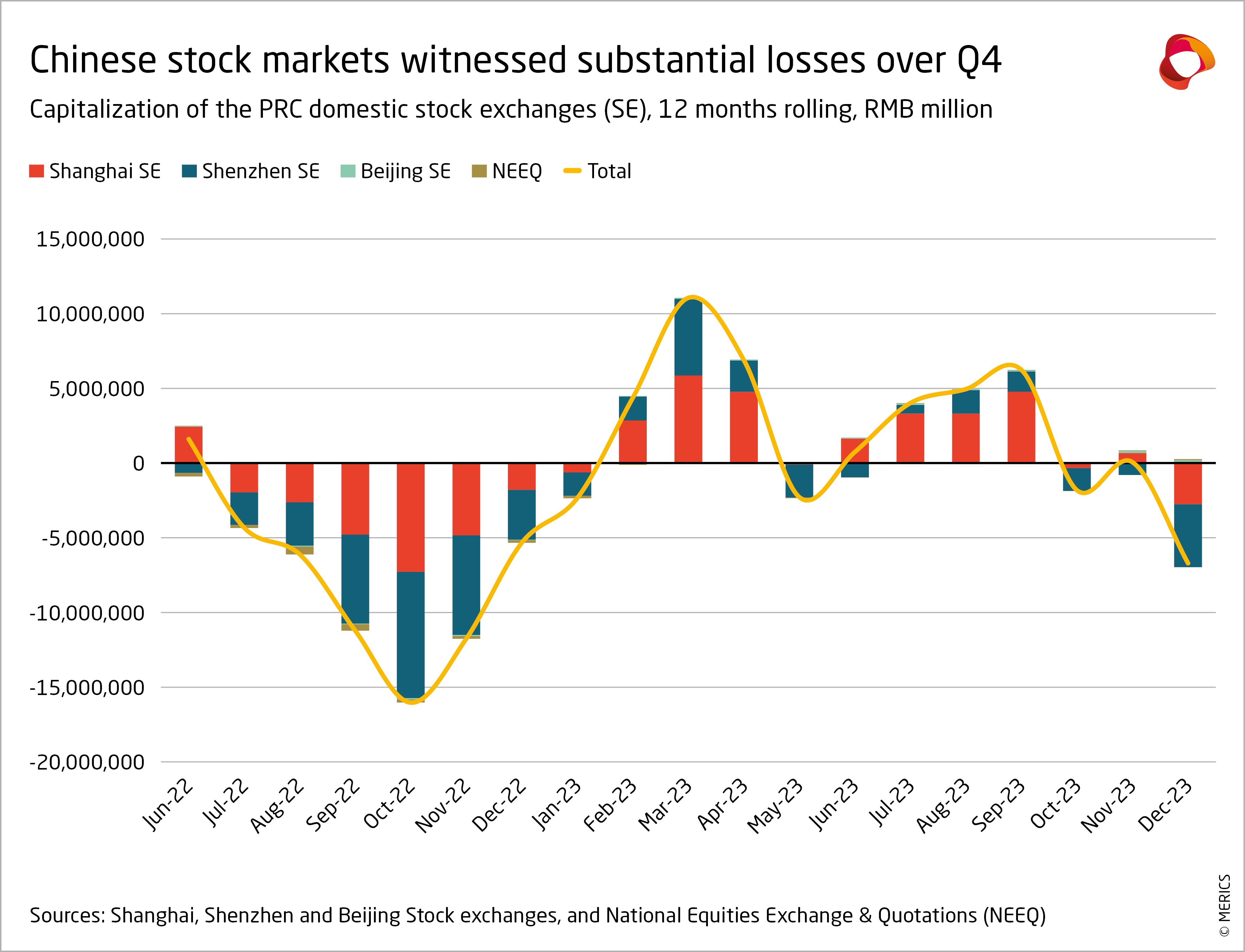

Exhibit 8

![]() Hover over/tap the charts to see more details.

Hover over/tap the charts to see more details.

- Looming deflation and escalating financial risks stemming from weak growth pushed policy makers to step up monetary support in Q4. The People’s Bank of China (PBOC) injected 1.7 trillion CNY into the financial system over the quarter, a level unseen since the turmoil of 2015 (see exhibit 8). Over 2024, the PBOC’s domestic balance-sheet grew by more than 20 percent.

- This effort succeeded in lowering rates on the financial markets by the end of the fourth quarter. As a result, bank’s net interest margins (the difference between rates on deposits and loans) reached an all-time low in Q3. Interest rates had shot up earlier in the quarter after financial troubles at a few financial institutions and the negative outlook on China’s sovereign credit rate given by Moody’s, a ratings firm.

- None of this has turned the tide. Households and SMEs remain reluctant to take on debt and invest. Household long term loans fell further, dropping by 7 percent year on year, despite low base effects in Q4 2022. Total social financing to the real economy accelerated, rising from 9.3 percent year on year at the end of Q3 to 9.8 at the end of the year. But this was only thanks to dynamic government debt and long-term credits to large corporates.

- Bond rates plummeted across the board in December after six months of increases. However, the improved financing environment has not spilt over into the real economy. Firms’ bond issuances remained extremely sluggish. Stock exchanges continued to bleed, with 2.5 trillion CNY of market capitalization erased over Q4 (see exhibit 9). Over 2024, mainland stock exchanges lost 7.5 trillion CNY of capitalization.

- Party-state economic documents setting out plans for 2024 signal further support to stabilize the economy. This coincides with the PBOC being politically downgraded and targeted by anti-corruption investigations. The central bank will therefore be less likely to temper pro-stimulus guidance from the top leadership in order to limit debt. Continuous upgrades to monetary support and an acceleration of debt dynamics are therefore the most likely scenarios for H1 2024.

What to watch: January credit data typically reflects an abnormal share of annual loans in China, so it will provide us with a better gauge of the Beijing’s more supportive stance in Q4 2023.

Investment: Investment remains suppressed by real estate sector’s woes

Exhibit 10

![]() Hover over/tap the charts to see more details.

Hover over/tap the charts to see more details.

Exhibit 11

- The real estate sector’s woes continue to weigh heavily on China's economy. Investments plummeted by 8 percent in December compared to a 5.1 percent fall at the end of Q1. Real estate investment has now been contracting since April 2022 with little optimism for a recovery any time soon.

- New building activity shows minimal improvement but remains dismal. Floor space under construction fell by 20.4 percent in December year on year (see exhibit 10). Economic activity in the sector could drop further in coming months as buildings currently under construction are completed.

- Overall investments will remain dampened by efforts to diversify away from the real estate sector. Growth in total fixed asset investments was up 3 percent at the end of Q4, compared to 5.4 percent during the same period in 2019 prior to the pandemic. However, December brought the first uptick in 2023, as growth edged up from 2.9 percent in November.

- The slight improvement was driven by increased investments in manufacturing, which were up 6.5 percent at the end of Q4 - the second highest performance since Q1, when growth was 7 percent. Manufacturing investment growth continued to be powered by investments electrical machinery (up 32.2 percent at the end of Q4) and automotive, up 19.4 percent.

- The private sector’s overall share of investment is declining rapidly, but it too continued to shift towards manufacturing (see exhibit 11). Private sector manufacturing investments rose by 9.1 percent in December, despite a fall in overall investment by private companies of 0.4 percent.

- The government has been holding back on rolling out infrastructure investments to stimulate investment. Investment increased by 5.9 percent at the end of Q4 compared to 9 percent in Q1. Rail investment continues to stand out, recording 25.2 percent growth in December, up from 1.8 percent a year ago.

What to watch: The key to greater economic stability is that the real estate sector needs to find its floor.

Prices: China dragged into deflation by persistent weak demand in Q4

Exhibit 12

![]() Hover over/tap the charts to see more details.

Hover over/tap the charts to see more details.

Exhibit 13

- China faced deflationary pressures in Q4 2023 as consumer prices slipped amid persistent weak demand. The annual consumer price index (CPI) recorded the lowest increase since 2009, plummeting to 0.2 percent, which is well below the government's 3 percent target.

- December CPI registered a slight improvement, at 0.3 percent. Even so, the monthly contraction was still the sharpest decline since February 2009. Deflationary pressure is likely to persist and may well push the government into more expansive policies in support of demand.

- Core inflation, which excludes volatile food and energy prices, managed to avoid deflation. It rose by 0.6 percent in December year on year. However, weak demand and deep rooted household insecurity was visible in the prices of durable consumer goods and households appliances, which contracted during most of 2023 (see exhibit 12).

- The producer price index (PPI) has now been contracting by 15 consecutive months. The slight improvement over the third quarter was not sustained throughout Q4. Producer prices contracted by 2.7 percent in December on year-earlier, slightly more than their 2.6 fall in October. On an annual basis, PPI fell by 3 percent, the strongest contraction since 2015.

- Falling real estate prices continue to be a primary factor in China's economic malaise, constraining consumption. The fourth quarter witnessed an increase in the share of cities reporting falling prices, rising to 68 percent from 60 percent at the end of the third quarter (see exhibit 13).

What to watch: Continuing deflation in the first quarter of 2024 would increase debt burdens and probably suppress consumption further.

Labor market: Weak employment conditions are dampening consumption

Exhibit 14

![]() Hover over/tap the charts to see more details.

Hover over/tap the charts to see more details.

Exhibit 15

- In a sluggish economy, companies are avoiding hiring and severely affected sectors, such as real estate, are laying off workers. This is creating a vicious circle as weak labor market conditions suppress consumption, which is needed for a recovery. Another record 11.9 million university graduates will enter the workforce this summer, so labor market pressure will persist in 2024.

- The government faces mounting pressure to bolster job opportunities to counter the dismal outlooks for future employment and wage growth (see exhibit 14). New measures to stabilize employment were rolled out throughout 2023 but had little effect. In the latest round, several local governments announced subsidies for new hires, and the Ministry of Education unveiled 26 measures to support graduate jobseekers.

- The challenging labor market was also evident in a surge of applicants seeking the safety of civil service jobs: a record 3 million took the entrance test in 2023 for a mere 39,600 openings (see exhibit 15).

- Companies are resorting to pay cuts to survive the weak economy. Even high-ranking executives in real estate and finance have had their pay trimmed. Job applicants who get hired can expect lower salaries. Average salaries were down by 1.3 percent in Q4 2023 compared to the same period of 2022, according to data compiled in 38 cities by online recruitment platform Zhaopin.

- By November (latest data available), a total of 11.8 million new urban jobs were created, up by 0.3 million from the same period year-earlier. While this was an improvement on 2022, it was 9.2 percent below pre-pandemic level with reports of under employment and risking number job seekers taking temporary job.

What to watch: The hiring season after Chinese New Year in mid-February will provide the first indication of the labor market in 2024.

Retail: Households are still wary about returning to old spending patterns

Exhibit 16

![]() Hover over/tap the charts to see more details.

Hover over/tap the charts to see more details.

Exhibit 17

- After five months of steady increases, retail sales expanded again in November, up by 10.1 percent year on year, which was their second highest growth rate in 2023. However, the recovery remains fragile as growth fell to 7.4 percent in December, below market expectations of 8 percent. Annual retail sales growth was 7.2 percent.

- Retail spending did improve in 2023, after a 3-year slump, but spending has yet to normalize to pre-Covid levels (see exhibit 16). Total sales revenue reached 47 billion CNY and remains roughly 10 percent below pre-pandemic expectations.

- Household sentiment remains negative, according to the National Bureau of Statistics’ (NBS) consumer sentiment index. The sub-index on willingness to spend stagnated at low levels; in December it was 89.2, with values below 100 indicating a negative outlook. Consumption will only improve consistently when sentiment does.

- Vehicle sales have held up well, growing more than 10 percent in Q4 compared to the same three months of 2022. By contrast, sales of housing-related commodities such as appliances or furniture were subdued, reflecting the real estate sector’s struggles. These divergent trends show households are adjusting their spending behavior in a challenging economy.

- Growth in services continued to outperform physical goods (see exhibit 17). An uptick in travel and restaurant spending underpinned annual growth in retail services sales of 20 percent in 2024. Restaurant revenue also accelerated sharply over Q4, up 30 percent in December year on year, which was more than double the 13.8 percent growth at the end of Q3. Domestic travel also continued to surge, with growth of 104.8 percent in December on a year on year basis.

- In contrast to the boom in domestic travel, a recovery in international travel is still lagging. International air passenger volumes are improving but remain at 40 percent of pre-pandemic levels. The government has responded by easing visa restrictions for business and tourists to boost visitor numbers.

What to watch: Consumption will still need to pick up significantly to help lift the economy.

Autor(en)

Chief Economist

Senior Economist (Büro Brüssel)

Senior Analyst

Autor(en)

Chief Economist

Senior Economist (Büro Brüssel)

Senior Analyst