Tracker

Economic Indicators

China’s economy shows faint signs of stabilization over Q3

MERICS Economic Indicators Q3/2024

MERICS Q3 analysis: China’s economy shows faint signs of stabilization over Q3

The Chinese economy faced considerable challenges over the summer as the slump in the real estate sector continued weighing down consumer sentiment and added stress to local government finances. The country also battled severe heat and flooding, which hurt economic activity. Key economic indicators deteriorated sharply in July and August as a result, setting the stage for a disastrous Q3, which did not quite materialize, thanks to an unexpected rebound in September. In the end, Q3 GDP grew 4.6 percent, down only 0.1 points from the Q2 performance. Although not great, it put this year’s growth target of “around five percent” within reach.

China’s economy has now been in a nearly three-year slump, weighed down by a deepening contraction in the real estate sector, sluggish consumption, a weak labor market and entrenched deflation. As the year draws to a close, the leadership faces growing pressure to take action. Economic tensions continue to mount, despite progress towards the leadership’s strategic economic objectives, which put the focus on technology and growth in high-tech manufacturing.

The Politburo, the top decision-making body of the Chinese Communist Party (CCP), responded to the sluggish economy by announcing plans for more economic support. It followed up with a series of stimulus measures in September (and October) from the People’s Bank of China, the National Development and Reform Commission, and the Ministry of Finance, among others. These policy adjustments raised market expectations about the scale and scope of government intervention to lift the economy, which were soon disappointed.

Rather than pursuing growth at any cost, the stimulus aims to mitigate swelling risks. In light of an expected slowdown in exports and industrial production, a key goal is to stabilize GDP growth for 2025. To achieve this, the government must stabilize the tumbling real estate sector, which is the primary cause of local governments' fiscal distress and weak household sentiment holding back consumption.

While the stimulus acknowledges some of the economy’s challenges, the measures remain restrained compared to the scale of the headwinds. A more expansive fiscal package, including direct household support, has been hinted at but have yet to materialize. While more support is certainly on the cards, there is also a risk that the additional support will again fall short of market expectations.

These expectations stem from hopes for a return to pragmatism in China’s economic policies. However, under President Xi Jinping, the economy is undergoing a painful realignment from real estate toward technology, with economic weak spots tolerated as long as strategic objectives are met.

The recently announced stimulus measures highlight this focus on strengthening the industrial base and innovation. Balancing a booming tech sector with a struggling real estate market and increasingly distressed middle-class will be difficult in the coming months. But, for now, the pressure remains manageable, and policy adjustments are focused on managing both internal and external risks.

The MERICS China Confidence Index (MCCI)

The MERICS China Confidence Index measures household and business confidence in future income and revenues. The index is weighted between household and business indicators. It includes the following indicators: stock market turnover, future income confidence, international air travel, new manufacturing orders, new business in the service sector, urban households’ house purchase plans, venture capital investments, private fixed asset investments and disposable income as a share of household consumption. All components have been tested for trends and seasonality.

The MCCI was first developed in Q1 2017.

The MERICS China Confidence Index measures household and business confidence in future income and revenues. The index is weighted between household and business indicators. It includes the following indicators: stock market turnover, future income confidence, international air travel, new manufacturing orders, new business in the service sector, urban households’ house purchase plans, venture capital investments, private fixed asset investments and disposable income as a share of household consumption. All components have been tested for trends and seasonality.

The MCCI was first developed in Q1 2017.

![]() Hover over/tap the charts to see more details.

Hover over/tap the charts to see more details.

Exhibit 1

Macroeconomics: China’s GDP growth holds up relatively well in a challenging quarter

Exhibit 2

![]() Hover over/tap the charts to see more details.

Hover over/tap the charts to see more details.

Exhibit 3

- China's economy performed better than expected in Q3 2024, despite weak initial data in July and August. GDP growth slowed only slightly to 4.6 percent year-on-year, down from 4.7 percent in Q2, helped by improvements in key indicators in September. Although this suggests some stabilization, growth remains fragile and was in much need of the stimulus measures announced at the end of the quarter.

- In the first three quarters of this year, GDP growth expanded by 4.8 percent (see exhibit 1). However, the stimulus is unlikely to lift full year 2024 GDP growth above five percent. But as long as it reaches the lower levels of the government’s deliberately unspecific growth target of “around five percent” the outcome will be acceptable for the leadership, which puts more priority on achieving a tech-focused transformation of the economy than on mere growth alone.

- Nominal GDP growth has been below real GDP for six consecutive quarters as the economy battles with deflation. In the first six months of this year, nominal GDP grew 4.1 percent year-on-year, 0.7 points below real GDP.

- On a quarterly basis, GDP growth improved slightly, expanding by 0.9 percent in Q3, compared to 0.5 percent in Q2. Although below the 1.5 percent achieved in Q1, the marginal improvement does suggest that growth momentum is beginning to return, though it remains weak.

- Manufacturing growth slowed to five percent year-on-year in Q3, down from 6.2 percent in Q2. Despite this deceleration, the sector remains a key driver of the economy. Manufacturing growth over the first nine months has been strong relative to the past two years, helping to offset the deeper contraction in the real estate sector (see exhibit 2).

What to watch: The stimulus will soften the contraction in the real estate sector and should help stabilize the economy.

Business: Private sector benefits from China’s high-tech push

Exhibit 4

![]() Hover over/tap the charts to see more details.

Hover over/tap the charts to see more details.

Exhibit 5

- China’s industrial sector showed resilience in Q3, with manufacturing bouncing back from a July slowdown. Growth in September reached 5.2 percent year-on-year, lifting overall production expansion to six percent by the end of September. Growth remains significantly higher than the 4.2 percent recorded in Q3 last year, even though the pace has slowed since the beginning of the year.

- The key driver of growth was value-added production from domestic private companies, which have outpaced both state-owned enterprises and foreign-funded firms (see exhibit 1). Private companies are playing an increasingly central role in priority sectors such as batteries or machinery, reinforcing their importance for national tech and self-sufficiency objectives.

- New energy vehicles (NEVs) stood out within the private sector: value-added production of NEVs surged by 48.5 percent year-on-year in September, up from 37 percent at the end of Q2. There was also significant growth in other tech sectors, such as solar cells and industrial robots, highlighting the shift towards higher value-added production (see exhibit 2).

- The boom in technology-related sectors had a positive impact on business sentiment. The purchasing managers' index (PMI) for high-tech manufacturing jumped from 49.9 in July to 53 in September, with values above 50 indicating expansion. However, overall manufacturing PMI showed little improvement, rising only slightly from 49.4 to 49.8, suggesting that growth is concentrated in specific sectors.

- Despite robust production figures, industrial profits have not strengthened. In August, industrial profits contracted sharply, down by 17.1 percent year-on-year. While some of this decline can be attributed to high base effects from the previous year, weak pricing power in a deflationary environment is also eroding profitability.

What to watch: Exports are likely to cool further, which is one reason behind the government’s stimulus measures aimed at safeguarding GDP growth in 2025.

International trade and investment: Exports are losing their ability to prop up China’s economic growth

Exhibit 6

![]() Hover over/tap the charts to see more details.

Hover over/tap the charts to see more details.

Exhibit 7

- In Q3, exports expanded by over six percent year-on-year on a USD basis, a faster growth rate than in the previous two quarters of this year, thanks to a strong performance over the summer. In August, exports rose by 8.7 percent, the fastest pace of the year so far. However, export growth cooled to just 2.4 percent in September, despite weak growth in the comparison period of 2023 (-6.2 percent). The decline casts a shadow on exports as a reliable growth driver for the economy.

- Growing trade tensions are likely to become more consequential for China’s exports and could weigh down growth. For instance, the EU has imposed tariffs on electric vehicles (EV) ranging from 7.8 percent to 35.4 percent (on top of the existing ten percent) on various companies after an investigation. The US decision to ban China-linked vehicle technology is another sign of pushback.

- Passenger car exports have been especially strong this year, up by 28.9 percent in the first nine months, with EV exports up by 33.8 percent. Automotive exports have more than doubled when compared to the same period two years ago. But other areas have also recorded stronger growth, such as steel and ship exports (see exhibit 6).

- China's "new three" products—EVs, lithium batteries and solar cells—accounted for over four percent of total exports in the year to end-September. These high-value-added exports have played a key role in boosting trade, especially for the privately-owned companies that dominate those sectors (see exhibit 7).

- Imports, however, continued to underperform, expanding by just 0.3 percent in September. This reflected weak domestic demand, but also China's growing push for self-sufficiency. As a result, China's trade surplus rose by more than ten percent in the first nine months of 2024.

- Sectors with a previously strong import performance face challenges. Vehicle imports fell by 9.4 percent in the first nine months, while machine tool imports contracted by 11.8 percent, despite strong investment in China's manufacturing sector.

What to watch: Exports are likely to cool further, which is one reason behind the government’s stimulus measures aimed at safeguarding GDP growth in 2025.

Financial Markets: More monetary policy easing underway as credit growth struggles

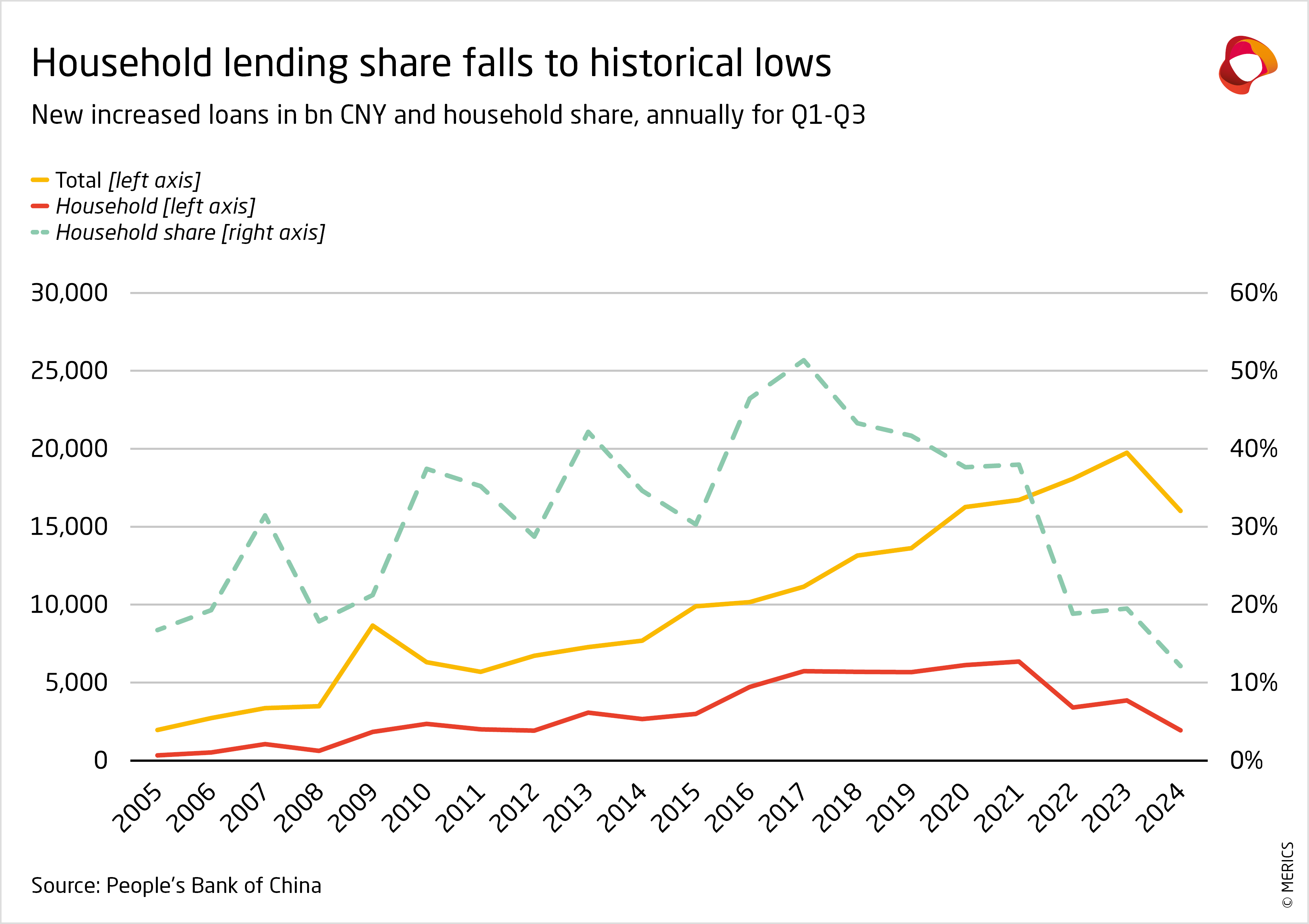

- The central bank’s efforts at cautious monetary easing over the first half of 2024 proved insufficient to boost the economy. The financing of the economy deteriorated substantially over Q3, putting the People’s Bank of China (PBOC) under fresh pressure to do more to support economic growth and battle increasingly entrenched deflation.

- Over Q3, weakening demand from households and corporates dragged down loan growth to an all-time low of 7.8 percent year-on-year at end-September, down from 8.3 percent at the end of Q2. Government bonds grew 16.4 percent year-on-year in September, reflecting the growth in trusted loans. Those geared towards improving financing for struggling real estate developers increased by 11.8 percent. These improvements only mitigated the slowdown; aggregate financing contracted by three percent in Q3.

- To reverse the trend, Beijing announced a large-scale monetary stimulus in late September. On top of the substantial 20 to 30 basis points reduction across policy rates, banks’ required reserve ratios (RRR) were also reduced to inject more liquidity. A dedicated refinancing facility was also created to support investment in the markets by financial institutions, with CNY 500 billion of capacity as a first batch. A second tranche of CNY 300 billion will be targeted at banks to finance equity injections and share buy-backs.

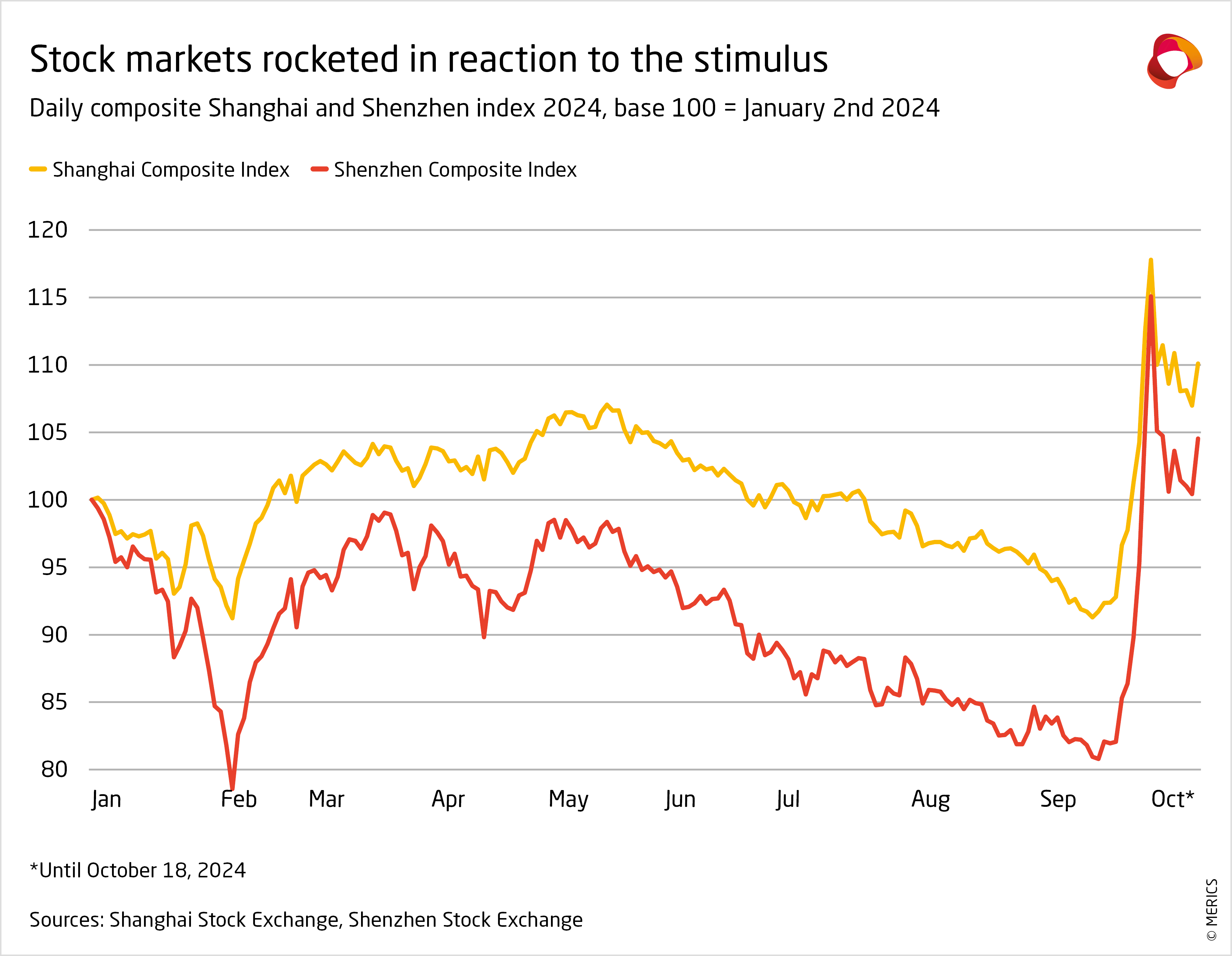

- The stimulus measures sent financial markets into a frenzy. In the week between 24-30 September, stock indices in Shanghai and Shenzhen rose by 21 percent and 30 percent respectively (see exhibit 8). This amounted to CNY 20 trillion in wealth creation, or roughly 15 percent of GDP. Markets started to ease again in early October as additional stimulus measures fell short of market expectations.

- Household credit demand is impacted by weak sentiment and a policy shift prioritizing investment in manufacturing and technology. New loans in the first nine months match 2012 levels, despite GDP more than doubling since then (see exhibit 9).

What to watch: Without a more far-reaching, structural stimulus package, the financial support measures are unlikely to shore up sentiment in a resilient way.

Exhibit 10

![]() Hover over/tap the charts to see more details.

Hover over/tap the charts to see more details.

Exhibit 11

- Over the course of the third quarter fixed asset investment (FAI) began to stabilize after slowing every month since March. In the first nine months to September investments increased by 3.4 percent, the same level as in the period until August. However, the overall average national figure masks different sectoral trends.

- Manufacturing investment grew by 9.2 percent over the first nine months, driven by China’s strategic shift towards technology and industrial self-reliance. This was slightly lower than 9.5 percent in the first half of the year. But despite the slowdown, investments geared towards strengthening China’s industrial foundations remain high (see exhibit 10).

- Overall private investment slipped back into contraction over Q3, yet manufacturing-related private investments expanded, underscoring the importance of privately-owned industrial firms for China's economic restructuring (see exhibit 11). Manufacturing-related investments expanded by 11.6 percent over the first nine months of 2024.

- Real estate investment slowed its rate of contraction for the first time this year but remains a major drag on overall investment. In the first nine months to end-September, real estate investment contracted by 10.1 percent, marginally better than the 10.2 percent contraction in the eight months before.

Ending the extended contraction of the real estate sector is a key objective of the stimulus measures rolled out in late September. The government’s measures included bringing down mortgage rates and more plans for the government to buy unsold housing inventory. - Investment in provinces in western China which typically have less manufacturing remained slack in Q3. Growth in the western provinces rose one percent compared to 3.8 percent in northeastern provinces, which benefit from investment in state-owned heavy industry. Regional disparities may widen as the government prioritizes high-tech manufacturing.

What to watch: Stabilizing the real estate sector is a key objective of the stimulus to put the economy on a more stable footing in 2025.

Prices: Deflation risks rise as prices cool

Exhibit 12

![]() Hover over/tap the charts to see more details.

Hover over/tap the charts to see more details.

Exhibit 13

- China’s economy has failed to shake off deflationary pressure with key price indicators softening over Q3. The government announced stimulus measures at the end of September to prevent deflation becoming entrenched. But persistent weakness in prices for real estate and industrial goods, coupled with subdued consumer sentiment, suggests the challenge of fighting deflation is far from over.

- Property prices have been on a downward trajectory for nearly six years now and contracting for three (see exhibit 12). In September, prices for new homes fell by 6.1 percent, the second largest contraction on record, overshadowed only by April 2015 when prices fell by 6.4 percent.

- Consumer price inflation (CPI) remained almost flat throughout the third quarter of 2024, as consumption stayed weak. Prices rises crept up by 0.5 percent in August - only slightly below the year’s peak so far of 0.7 percent in February – but they fell again to 0.4 percent in September. CPI rose by just 0.3 percent over the first nine months of 2024, which is well below Beijing’s three percent target.

- Core inflation, excluding more volatile energy and food prices, fell to just 0.1 percent in September. This was the lowest rise since February 2021. Prices rises for services slipped to 0.2 percent in September, the lowest level since March 2021.

- The purchasing price index (PPI) reversed the improvements seen in Q2, when prices contracted by just 0.8 percent. In Q3, PPI dropped by 2.8 percent. It was the sharpest quarterly contraction since Q1 2023. Any optimism that the PPI might stabilize has faded as China’s industrial sector continues to struggle with overcapacity and weak demand.

- Price falls for manufactured goods were particularly pronounced in the industrial sector. Prices had contracted by two percent at the end of Q2 year-on-year, and dropped further in September, down by 3.3 percent. This was due to a combination of overcapacity and weak demand for consumer goods, especially durable goods (see exhibit 13).

What to watch: The effectiveness of the latest stimulus measures will hinge on whether they can boost demand and lift price levels, but changes are unlikely to materialize before early 2025.

Labor Market: Government steps up support for sluggish labor market

![]() Hover over/tap the charts to see more details.

Hover over/tap the charts to see more details.

Exhibit 15

- Urban unemployment in China edged up slightly during the third quarter of 2024, rising from five percent in June to 5.1 percent by September. Despite the challenges it was still well below the six percent peak seen in 2022. Data on new urban employment signaled an improvement: 9.4 million jobs were created in the first eight months (latest data available) (see exhibit 14). However, employment data is not the full picture. People are suffering deeper concerns about income growth and job security and quality.

- Labor market sentiment, as tracked by the National Bureau of Statistics’ household survey, continued to show signs of weakening over Q3. Confidence in employment and income levels has been stuck at historic lows for nearly three years now, suggesting the labor market is still under pressure and weighing down household optimism.

- China’s government is tackling these challenges with new support measures aimed at stabilizing the labor market - again. The latest measures offer little more than previous ones. They may help stabilize the situation but are unlikely to bring significant improvements.

- In September, the State Council introduced a 24-point plan to encourage entrepreneurship and offer training and support for job seekers. Companies were incentivized to "fulfill their social responsibilities" by creating jobs with the support of tax and social security cuts. But without a stronger economic recovery these measures feel largely symbolic. Substantial improvements in the labor market are unlikely for now.

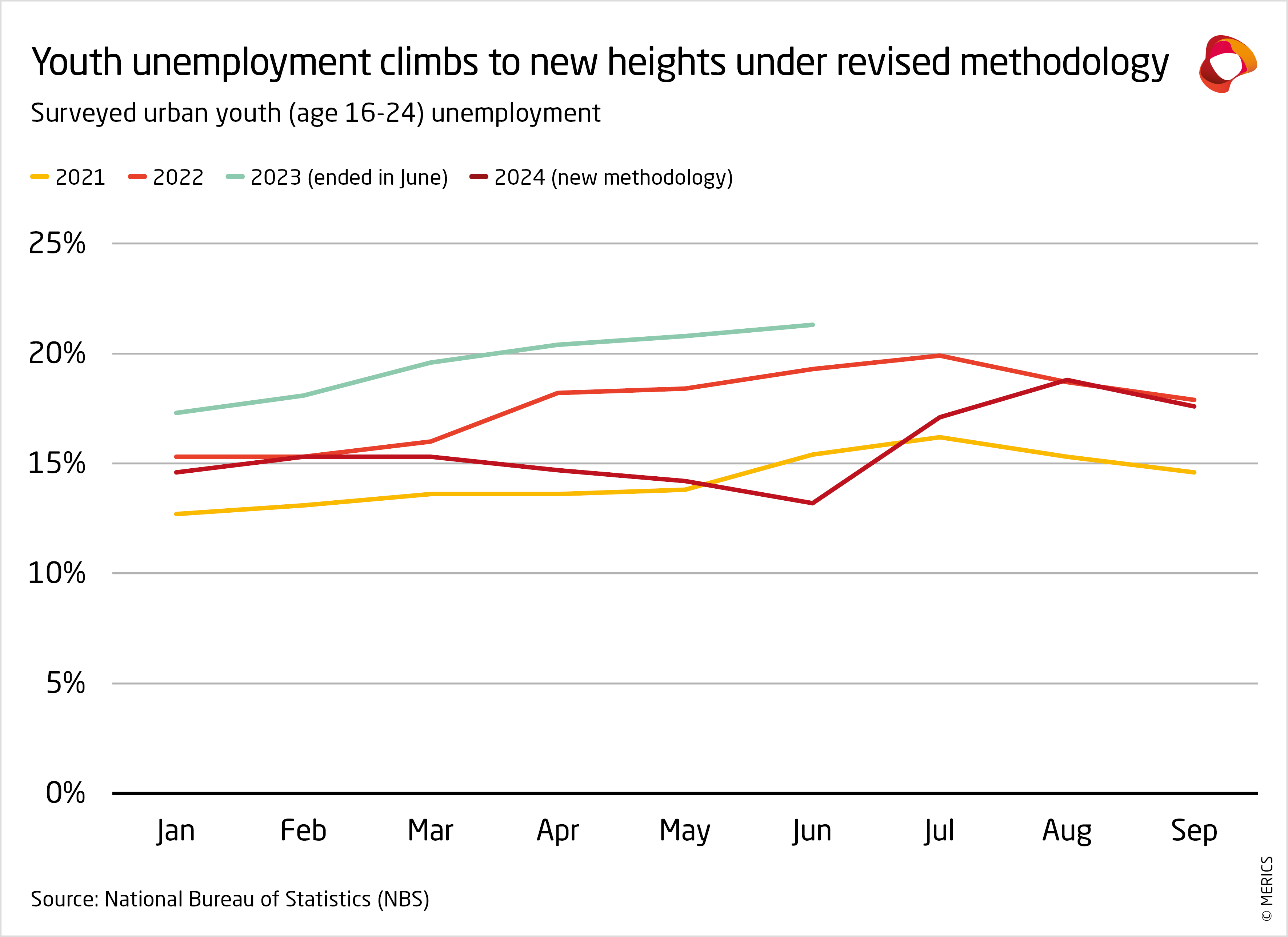

- Additional support was allocated for vulnerable groups, particularly migrant workers, retired military personnel and university graduates, who continue to face problems finding employment. Youth unemployment hit a record high of 18.8 percent in August, following a statistical revision by the National Bureau of Statistics and remains high despite an improvement in September (see exhibit 15).

What to watch: Real improvements in employment and income are needed for household sentiment to improve and drive up consumption.

Retail: A September rebound in consumption offers some hope

Exhibit 16

![]() Hover over/tap the charts to see more details.

Hover over/tap the charts to see more details.

Exhibit 17

- Consumption remained under pressure in Q3, with retail spending offering a mixed picture. Retail sales picked up pace in September after weak growth in the first two months. September growth beat market expectations, rising by 3.2 percent year-on-year, up from a sluggish 2.1 percent in August. While the September rebound offers a glimmer of hope, it was not strong enough to signal a broader turnaround in consumer activity.

- Stronger urban spending played a significant role in the September recovery, with growth rising to 3.1 percent from 1.8 percent in August. Rural spending, which consistently outperforms urban spending, expanded by 3.9 percent in September. However, rural consumption only accounts for about 15 percent of total retail sales, limiting its broader impact.

- Total retail growth continued to slip when measured over the first nine months of 2024. Retail spending had risen by 3.3 percent at the end of Q3, down from 3.6 percent at the close of Q2. Over the quarter, slower growth was reported in all segments, including spending on services (see exhibit 16).

- Sales of home appliances surged by 20.5 percent in September in response to a trade-in program launched at the end of August (see exhibit 17). The Ministry of Commerce has offered subsidies of up to CNY 2,000 on eight kinds of home alliance to encourage upgrades to higher energy efficiency models.

- Stimulus measures were expanded substantially in September in order to boost consumption further. Against a backdrop of weak sentiment and labor market insecurity, it is doubtful if they will be enough to counter the impact of these factors. The National Bureau of Statistics’ consumer confidence index failed to improve, falling to 85.8 in August (latest data available), down from 86.2 in June.

What to watch: Household sentiment will need to improve for consumption growth to get onto a more stable footing.

Autor(en)

Chief Economist

Senior Economist (Büro Brüssel)

Senior Analyst

Autor(en)

Chief Economist

Senior Economist (Büro Brüssel)

Senior Analyst