picture alliance / CFOTO

Comment

The e-CNY will not help the yuan displace the dollar any time soon

The digital yuan promises China a sanctions-proof payments system and more power to monitor international transactions. François Chimits does not expect a flood of foreign users.

The People’s Bank of China (PBoC) has pledged to “explore the improvement of cross-border payments” with the country’s nascent digital currency, causing some alarm in the West that the e-CNY may revive the flagging internationalization of the yuan. The country’s central bank has launched pilots with Hong Kong, Thailand and the United Arab Emirates, its commercial banks have promised infrastructure and Xi Jinping likes to talk about international partners. But the e-CNY will not remove the obstacles hindering the yuan from challenging the dollar – and new features it brings to international transactions look set to deter many users.

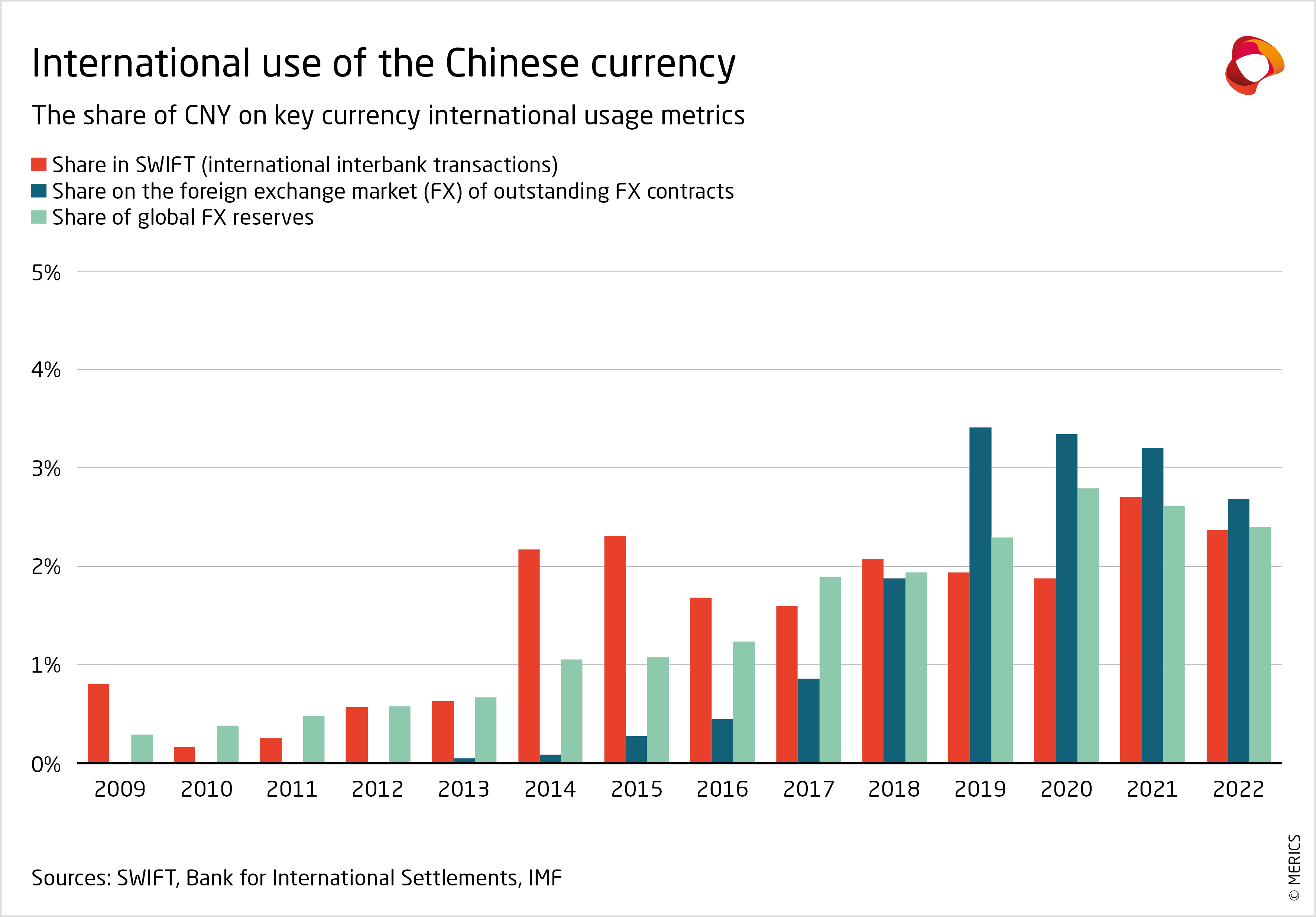

The internationalization of the yuan has stalled in recent years (see Exhibit 1) and even Chinese experts say that a currency becomes useful beyond its borders only if it can meet three conditions: accessibility, availability and trust. The yuan has taken a leap to fulfilling the first criterion as Chinese financial markets have become easily accessible to international investors through the “stock connect” trading links to Hong Kong. Chinese securities are now included in leading international financial indexes and reforms have improved the liquidity and depth of the bond market, popular with foreign investors looking for safe assets.

While this led to massive inflows of money from abroad, the other two criteria still blocked any significant advances in internationalizing the yuan. Recent years have seen China’s current account swing back into surplus, meaning the other countries of the world saw a net outflow of yuan as they paid for all their Chinese imports. Constrained global availability of the yuan is likely to continue given Beijing’s official objective of maintaining an industrial share of gross domestic product (GDP) akin to those of countries with big trade surpluses.

At the same time, trust has hardly improved. Despite significant reforms of China’s financial and legal framework, the predictability and the transparency of the country’s financial system has hardly improved. Foreign-exchange management was outsourced to state-owned banks in completely opaque ways. Chinese monetary policy has returned to using more opaque instruments. And, more broadly, there is a widely shared perception of a more ideologized political environment that has done nothing to foster the trust of international investors.

The virtual currency won’t make up for the yuan’s acceptance problems

The e-CNY looks extremely unlikely to appreciably increase foreign access to or trust in the yuan. Chinese officials have conspicuously avoided linking the digital currency to yuan internationalization – former PBoC governor Zhou Xiaochuan has said the e-CNY “can greatly raise levels of convenience“, but that it or its peers would not become a “world unifier”. The latest Chinese central bank report about yuan internationalization did not mention the digital currency, while a report on the digital CNY said nothing about currency internationalization.

Beyond a genuine ability to lower transaction costs, cross-border transactions in e-CNY would most immediately benefit the Chinese party-state. It could help better shield transacting companies and their respective countries from sanctions, especially the long-arm jurisdiction of the USA. Washington draws considerable power from there being no real alternative to SWIFT, the monopolistic international interbank payments system that abides by US sanctions. Sanctioned entities and any companies that choose to do business with them can be banned from SWIFT, making international transactions extremely cumbersome to clear and settle.

The e-CNY, like other digital currencies, could provide companies and countries not aligned with US sanctions a safe alternative to SWIFT. But avoiding secondary sanctions in this way would come at a price, as any entities willing to use alternative international payments systems would presumably have to forego any type of dollar financing going forward. Nevertheless, this feature of digital currencies has been a strong driver of support in the Chinese discussion and has even been underlined by high-level Russian financial officials.

The e-CNY will pay a price if it is used to evade sanctions and monitor transactions

Cross-border e-CNY transactions would also improve Beijing’s ability to fight illegal financial flows. That is because what the PBoC calls the “controllable anonymity” of the Chinese digital currency gives authorities the technical means to scrutinize transactions they deem suspicious and identify the counterparties. International users of the e-CNY would, fairly or unfairly, risk becoming the target of Chinese repressive system. The tool is particularly appealing to a country that has tight capital controls – and hundreds of billions of USD of illegal outflows.

But for Beijing, using the e-CNY to evade sanctions and monitor international transactions would not come cost free. Companies that used the digital yuan to trade with entities under primary sanctions from the US would run the risk of being targeted by secondary sanctions in the form of exclusion from US dollar-denominated international payments. And the more Beijing used its power to monitor e-CNY transactions, the more uneasy foreign users would become. Under these circumstances, it’s hard to see how the digital yuan will help the Chinese currency become a major global trading and reserve currency like the dollar any time soon.

Author(s)

Senior Economist (Brussels office)

Author(s)

Senior Economist (Brussels office)